Compound Interest Calculator USA

Discover the eighth wonder of the world – watch your money multiply while you sleep. Free, accurate, and built for American investors.

What Is the Compound Interest Calculator USA?

Let's be honest – watching your bank account grow feels pretty damn good. But here's the thing: most Americans don't realize just how powerful their money can become when they let compound interest do its magic.

Our Compound Interest Calculator USA isn't just another boring financial tool. It's your personal wealth-building crystal ball. Whether you're saving for retirement, your kid's college fund, or that dream vacation home in Florida, this calculator shows you exactly where your money's headed.

🎯 Built for Americans

Designed specifically for US tax brackets, contribution limits, and investment vehicles like 401(k)s and IRAs.

💰 Real-Time Projections

See instant results as you adjust your numbers. No waiting, no confusion – just pure financial clarity.

📊 Visual Growth Charts

Watch your money grow with beautiful, easy-to-understand graphs that make compound interest click.

How Does Compound Interest Actually Work?

Here's the beautiful part about compound interest: your money makes money, and then that new money makes even more money. It's like a snowball rolling down a hill – starts small, but gets bigger and faster as it goes.

The Magic Formula Behind Your Wealth

When you invest $10,000 at 7% annual return, you don't just earn $700 the first year. In year two, you earn 7% on $10,700. By year ten, you're earning interest on interest on interest. That's the compounding effect, and it's why Einstein supposedly called it the eighth wonder of the world.

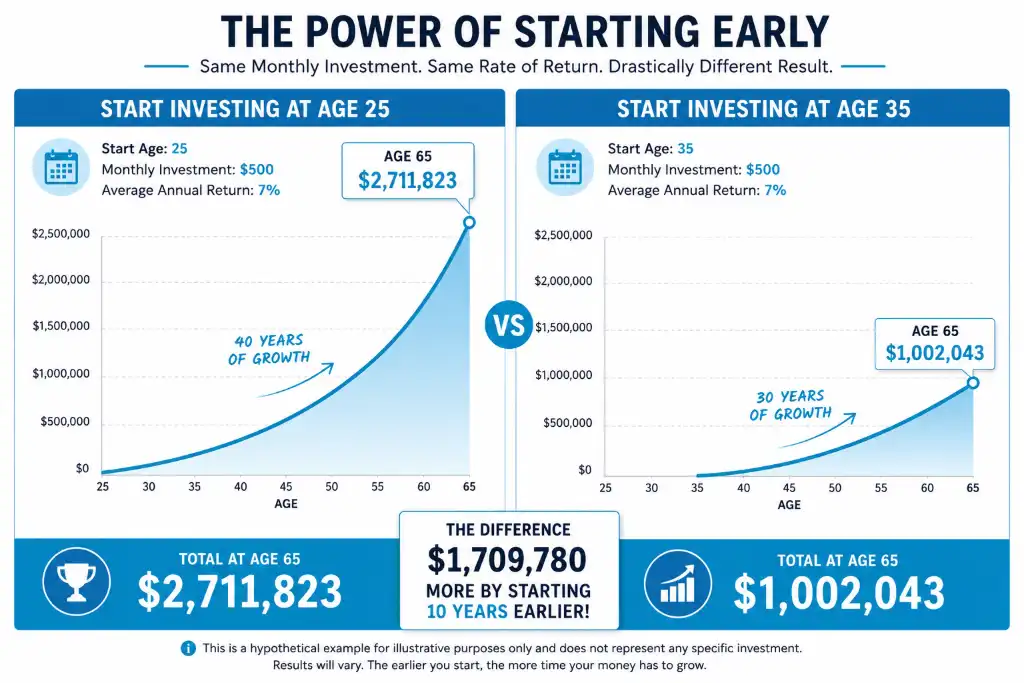

Why Timing Beats Timing the Market

Sarah started investing $300 monthly at age 25. Her friend Mike waited until 35 to start investing $500 monthly. Guess what? Even though Mike invested more money overall, Sarah ended up with significantly more at retirement. Why? She gave compound interest an extra decade to work its magic.

Monthly Compound Interest Calculator with Contributions USA

Most of us aren't sitting on a huge lump sum to invest. We're regular folks with regular paychecks. That's why our monthly compound interest calculator with contributions USA focuses on what really matters: consistent, monthly investing.

Why Monthly Contributions Change Everything

Think about your 401(k) or IRA. You're probably contributing a chunk from each paycheck, right? That's dollar-cost averaging in action, and it's one of the smartest moves you can make.

The Power of "Set It and Forget It"

- Automatic discipline: Money leaves your account before you can spend it

- Market volatility protection: You buy more shares when prices are low, fewer when high

- Compound acceleration: Each contribution starts earning immediately

Real Numbers: What $200/Month Really Becomes

Let's get specific. You invest $200 monthly for 30 years at an average 8% return (pretty conservative for the S&P 500). Here's what happens:

Year 10

Total Invested: $24,000

Account Value: $36,800

Interest Earned: $12,800

Year 20

Total Invested: $48,000

Account Value: $118,400

Interest Earned: $70,400

Year 30

Total Invested: $72,000

Account Value: $298,900

Interest Earned: $226,900

See that? In the final decade, your interest earnings alone exceed your total contributions. That's the hockey stick effect of compound growth.

How Much Will My Savings Grow? Calculator USA Yearly Returns

You're probably wondering: "Okay, this sounds great, but how much will MY savings actually grow?" That's exactly what our calculator answers. Plug in your numbers and watch the future unfold.

Understanding Yearly Returns vs. Monthly Compounding

Here's something that trips people up: the difference between annual percentage rate (APR) and annual percentage yield (APY). When interest compounds monthly, your actual yearly return is slightly higher than the stated rate.

The Math That Makes You Richer

If your investment earns 6% annually but compounds monthly, your effective annual yield is actually 6.17%. Doesn't sound like much? Over 30 years on a $50,000 investment, that extra 0.17% adds up to an additional $8,500. Not bad for doing absolutely nothing.

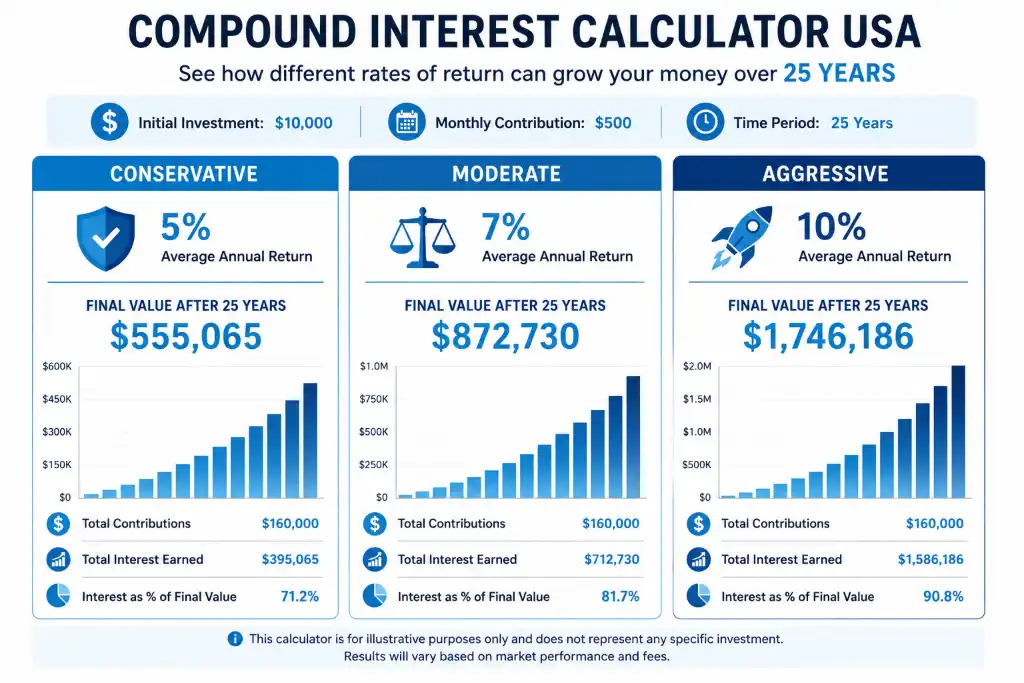

Conservative vs. Aggressive Growth Scenarios

Let's say you have $25,000 to invest today and can add $400 monthly. Here's how different return rates affect your 25-year outcome:

- Conservative (5%): $295,000 total value

- Moderate (7%): $425,000 total value

- Aggressive (10%): $665,000 total value

That 5% difference between conservative and aggressive? It's an extra $370,000. This is why asset allocation matters so much, especially when you're young and can afford to take calculated risks.

Retirement Planning Made Simple

Retirement might feel like a lifetime away, but here's the brutal truth: the average American needs about $1.5 million to retire comfortably. Scary? Maybe. Achievable? Absolutely – if you start now.

401(k) vs. IRA: Which Compound Interest Vehicle Wins?

Both accounts let your money compound tax-advantaged, but they work differently:

Traditional 401(k) & IRA

- Contributions reduce your taxable income today

- Money grows tax-deferred

- You pay taxes on withdrawals in retirement

- 2026 contribution limit: $23,000 for 401(k), $7,000 for IRA

Roth 401(k) & IRA

- Contributions are after-tax (no immediate deduction)

- Money grows completely tax-free

- Qualified withdrawals in retirement are 100% tax-free

- Same contribution limits as traditional

Here's the kicker: if you're in the 22% tax bracket now and expect to be in the same bracket in retirement, a Roth IRA could save you six figures over your lifetime. Why? Because all that compound growth happens tax-free.

The Employer Match: Free Money You Can't Ignore

If your employer offers a 401(k) match and you're not maxing it out, you're literally leaving money on the table. A 50% match on 6% of your salary is an instant 50% return on your investment. Where else can you get that?

Example: You make $60,000 and contribute 6% ($3,600/year). Your employer adds $1,800. That's $5,400 going into your account for just $3,600 out of pocket. Over 30 years at 7% return, that employer match alone grows to over $400,000.

Real-Life Success Stories

Numbers on a screen are one thing. Real people achieving real results? That's inspiring. Here are actual scenarios our calculator has helped people plan:

The Late Starter (Age 45)

Maria realized at 45 she had only $50,000 saved. Panic mode? Not quite. She started contributing $1,200 monthly to her 401(k), got a 4% match, and earned 7% annually. By 67, she had $890,000. Not the $1.5 million she wanted, but combined with Social Security, she's set.

The Early Bird (Age 22)

Jake started right out of college with just $150 monthly. Small, right? But by increasing his contribution 3% yearly (matching his raises), he'll have over $1.2 million by 62. The lesson? Start small, but start NOW.

The Aggressive Saver (Age 35)

The Chen family maxed out both 401(k)s ($46,000/year combined) plus two IRAs ($14,000). At 8% return, they'll have $3.2 million by 65. Their secret? Living below their means and letting compound interest do the heavy lifting.

Advanced Strategies to Supercharge Your Returns

Once you understand the basics, it's time to level up. These strategies can add hundreds of thousands to your final number:

1. The Roth Conversion Ladder

Convert traditional IRA funds to Roth IRA strategically over several years. You pay taxes now at your current rate, but all future growth is tax-free. Perfect if you expect tax rates to rise (and let's be real, they probably will).

2. Mega Backdoor Roth

If your 401(k) allows after-tax contributions, you can potentially stuff an extra $30,000+ per year into a Roth. This is an advanced move, but it can add $2 million+ to your retirement over 30 years.

3. Tax-Loss Harvesting

Sell losing investments to offset capital gains, then immediately buy similar (but not identical) investments. You maintain your market position while creating tax deductions. Those saved taxes? Reinvest them and watch them compound too.

Want to calculate loan payments for that investment property you're considering? Check out our EMI Calculator to see if the numbers make sense.

Common Mistakes That Kill Compound Growth

Even smart people mess this up. Don't be one of them:

Mistake #1: Cashing Out Early

That $20,000 401(k) withdrawal for a down payment? It's not just $20,000. It's $20,000 that would have grown to $160,000 in 30 years. Plus penalties and taxes. Ouch.

Mistake #2: Playing It Too Safe

Keeping everything in bonds or money market accounts might feel safe, but inflation eats 3% yearly. Your "safe" 4% return is actually 1% real growth. Over decades, that's the difference between retirement and working forever.

Mistake #3: High Fees

A 1% expense ratio doesn't sound bad. But over 40 years, it can consume 25% of your potential returns. Stick to low-cost index funds (0.1% or less) and watch the difference compound.

Thinking about buying a car? Use our Auto Loan Calculator with Credit Score USA to see how financing affects your wealth-building timeline.

Tools That Work Together

Compound interest is powerful, but it's part of a bigger financial picture. Here's how to use multiple tools strategically:

The Wealth-Building Stack

- Start with budgeting: Know where your money goes

- Use our Compound Interest Calculator: Project your investment growth

- Plan systematic investments: Set up automatic contributions with our Systematic Investment Plan calculator

- Manage debt wisely: Don't let high-interest debt derail your compounding

- Reassess yearly: Adjust contributions as income grows

Frequently Asked Questions

The Rule of 72 is a quick mental math trick: divide 72 by your annual return rate to see how many years it takes to double your money. At 8% return, your investment doubles in 9 years (72 ÷ 8 = 9). At 6%, it takes 12 years. It's not exact, but it's surprisingly accurate for returns between 6-10% and helps you grasp compound interest without a calculator.

Absolutely, and the difference is staggering. With simple interest, you only earn on your original principal. With compound interest, you earn on principal PLUS accumulated interest. On a $10,000 investment at 7% for 30 years: simple interest gives you $31,000 total, while compound interest gives you $76,123. That's $45,000 extra just from compounding.

Daily compounding gives you the highest return, but the difference between daily and monthly is minimal. For example, $10,000 at 6% for 20 years: annually compounded = $32,071, monthly = $33,102, daily = $33,196. The real game-changer isn't compounding frequency – it's starting early and contributing consistently.

Yes, if you invest in volatile assets like stocks. Compound interest works both ways – losses compound too. However, historically, the S&P 500 has never had a negative 20-year period. The key is time horizon: if you need money in 3 years, don't invest it in stocks. If you have 20+ years, short-term volatility becomes irrelevant.

APR (Annual Percentage Rate) is the simple interest rate without compounding. APY (Annual Percentage Yield) includes the effect of compounding. If your account earns 6% compounded monthly, the APR is 6%, but the APY is 6.17%. Always compare APY when evaluating savings accounts or investments – it shows your true return.

It depends on the interest rate. If your credit card charges 18%, paying it off guarantees an 18% return – better than any investment. But if your mortgage is 4% and you can earn 8% in the market, investing wins. Rule of thumb: pay off high-interest debt (>7%) first, then invest aggressively.

Inflation is the silent killer of compound growth. If you earn 7% but inflation is 3%, your real return is only 4%. Over 30 years, $100,000 growing at 7% nominal becomes $761,000, but in today's purchasing power, it's worth about $314,000. Always calculate using "real returns" (nominal return minus inflation) for realistic planning.

Be conservative. While the S&P 500 averages 10% historically, that includes dividends and doesn't account for inflation. For planning: use 6-7% for stock-heavy portfolios, 4-5% for balanced portfolios, and 3-4% for conservative portfolios. It's better to be pleasantly surprised than disappointed.

Yes, but it takes time and consistency. Investing $300 monthly at 8% return: after 10 years = $54,000, after 20 years = $176,000, after 30 years = $447,000, after 40 years = $1.05 million. The first decade feels slow, but years 30-40 add more than the first 30 combined. Patience is everything.

It depends on the account type. In taxable accounts, you pay taxes yearly on interest, dividends, and capital gains – this slows compounding. In tax-advantaged accounts (401k, IRA), growth compounds tax-deferred or tax-free. Roth accounts are especially powerful: you pay taxes upfront, but all compound growth is tax-free forever.

Your money keeps compounding! This is crucial. If you invest $500 monthly for 15 years ($90,000 total) at 8%, then stop contributing but leave it invested for another 20 years, you'll have $1.1 million at year 35. Your money worked harder in the 20 years you didn't contribute than in the 15 years you did.

Absolutely not. While starting early is ideal, compound interest still works powerfully at 50. If you invest $1,500 monthly for 15 years at 7%, you'll have $485,000. Add catch-up contributions (available after 50): you can contribute $30,500/year to a 401(k) instead of $23,000. Every year counts.

Short-term pain, long-term gain. During crashes, your account value drops, BUT your monthly contributions buy more shares at lower prices. When the market recovers (and it always has), those discounted shares supercharge your returns. The 2008 crash looked terrifying, but investors who kept contributing through 2009-2010 saw massive gains by 2015.

Use it for everything! Retirement is obvious, but also calculate for: college savings (529 plans), house down payments, emergency funds, business capital, or financial independence. The math is the same – only the time horizon and risk tolerance change. Short-term goals (under 5 years) should use conservative returns; long-term goals can be more aggressive.

Waiting to start. Every year you delay costs you exponentially. Starting at 25 vs. 35 doesn't just cost you 10 years of contributions – it costs you 10 years of compounding on those contributions, plus compounding on that compounding. The difference between starting at 25 vs. 35 with $400/month at 8%? Over $600,000 by age 65. Start today, even if it's just $50.

Our calculator assumes regular monthly contributions for simplicity, but real life isn't always regular. If you get bonuses, tax refunds, or irregular income, calculate your average monthly contribution. For example, if you invest $5,000 yearly but irregularly, use $417/month in the calculator. It won't be exact, but it'll be close enough for planning.

Ready to See Your Financial Future?

Stop guessing. Start knowing. Use our free Compound Interest Calculator USA right now and discover exactly where your money's headed.

Your future self will thank you.

Calculate My Growth Now